The valuation of intangible assets (patents, human capital, know-how) is the true engine of emerging technological sectors. A landmark joint study published in December 2025 by the Organisation for Economic Co-operation and Development (OECD) and the European Patent Office (EPO) provides an exhaustive mapping of the global quantum ecosystem.

Through the analysis of patent data, investments, and skills, this report demonstrates that quantum technologies (computing, communication, and sensors) represent a fascinating case study for professionals in intangible asset valuation. Below are the highlights of this study, supported by precise figures.

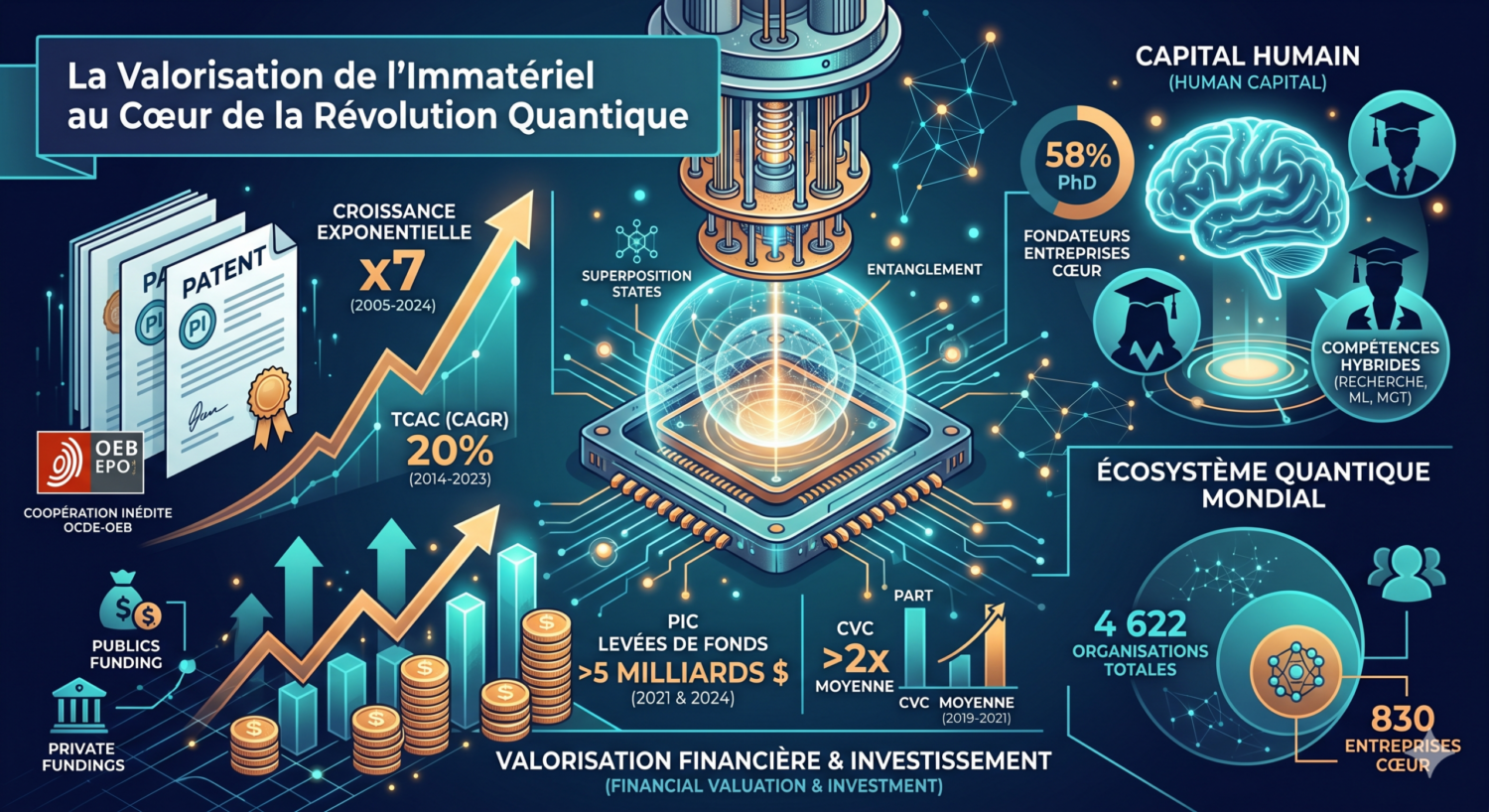

1. Intellectual Property (IP): An Early Indicator of Value Creation

In a field where commercial maturity is still low, patents constitute the primary form of innovation valuation. The study reveals hyper-growth in the creation of IP assets:

- Exponential Growth: The number of International Patent Families (IPFs) in the quantum field increased sevenfold between 2005 and 2024. Between 2014 and 2023, these patents experienced an exceptional Compound Annual Growth Rate (CAGR) of 20%, far outstripping the 2% observed across all other technological fields.

- Highly Strategic Assets: Quantum innovators show a strong propensity to protect their assets internationally. The patent internationalization rate is 31.2%, compared to an average of only 12% for all patents.

- Science/Industry Hybridization: The proximity between fundamental research and industrial valuation is striking. Approximately 33% of citations in quantum patents refer to non-patent literature (scientific articles), which is three times higher than the rates observed in medical technology and significantly higher than in classical computing sectors.

2. Human Capital: A Barrier to Entry and a Priceless Intangible Asset

The development of the ecosystem relies on a rare concentration of talent and hyper-specialized skills. When valuing a quantum company, the quality of its human capital is an essential criterion.

- Extraordinary Educational Standards: Founders of specialized quantum companies (“core firms”) possess atypical academic profiles. 58% of them hold a PhD, compared to only 10% in the general startup founder population.

- Demand for Hybrid Skills: Job postings reflect a need for advanced technical skills (research is mentioned in 78% of recent ads, machine learning in 33%), but also an increasing integration of transversal skills such as communication (45%) and management.

- Business Creation Asymmetry: The ecosystem remains hyper-concentrated. Out of 4,622 identified organizations, only 830 are “core” companies whose primary activity is quantum. The remainder (over 80%) consists of large tech corporations or public research centers diversifying their portfolios. Furthermore, 20% of patent holders concentrate 75% of all filed quantum patents.

3. Financial Valuation: Investment Dynamics and the Role of the State

The financial translation of these intangible assets can be read through fundraising and market dynamics.

- Massive but Polarized Capital: Investment has seen strong growth, peaking at nearly $5 billion raised in 2021 and again in 2024. However, the ecosystem is geographically unbalanced: the United States captures approximately 60% of global funding, despite accounting for only about 30% of patents (IPFs) and startups.

- Strategic Interest from Large Groups (CVC): Quantum valuation is heavily attracting Corporate Venture Capital (CVC). The share of CVC in quantum funding reached 8% between 2019 and 2021—more than double the share of CVC in general startup investments. This illustrates the desire of large corporations to acquire or align themselves with this disruptive technology.

- Crucial State Support: Given the technological risk (with Technology Readiness Levels still low), private capital is not enough. Public authorities are involved in 25% to 35% of investment transactions. Additionally, the share of quantum R&D in OECD countries’ public R&D budgets rose from 0.4% in 2015 to 1.1% in 2023.

Conclusion

The 2025 mapping of the quantum ecosystem proves that we are witnessing a global race for intangible assets. For valuation professionals, the quantum sector perfectly illustrates the need for a multi-criteria approach: it is no longer about valuing existing cash flows (which are often non-existent at this stage), but rather assessing the strength of patent portfolios (IP), the scarcity of human capital (PhDs), and strategic positioning within an ultra-concentrated supply chain.